October 14, 2025

If your San Diego–based company pays dividends or interest to foreign investors, the default 30% U.S. withholding under IRC §§1441/1442 can be reduced or even eliminated when you plan ahead. Here’s a quick, practical framework our Carlsbad CPA team uses to help clients optimize cross-border withholding on U.S. Dividends and Interest while staying fully compliant.

✅ Identify the payee and the income type.

Portfolio dividends, qualified dividends, interest (including OID), and bank deposit interest are treated differently. Confirm whether the recipient is an individual, company, partnership, or disregarded entity, and whether there’s a “look-through” requirement.

✅Collect accurate W-8s before payment.

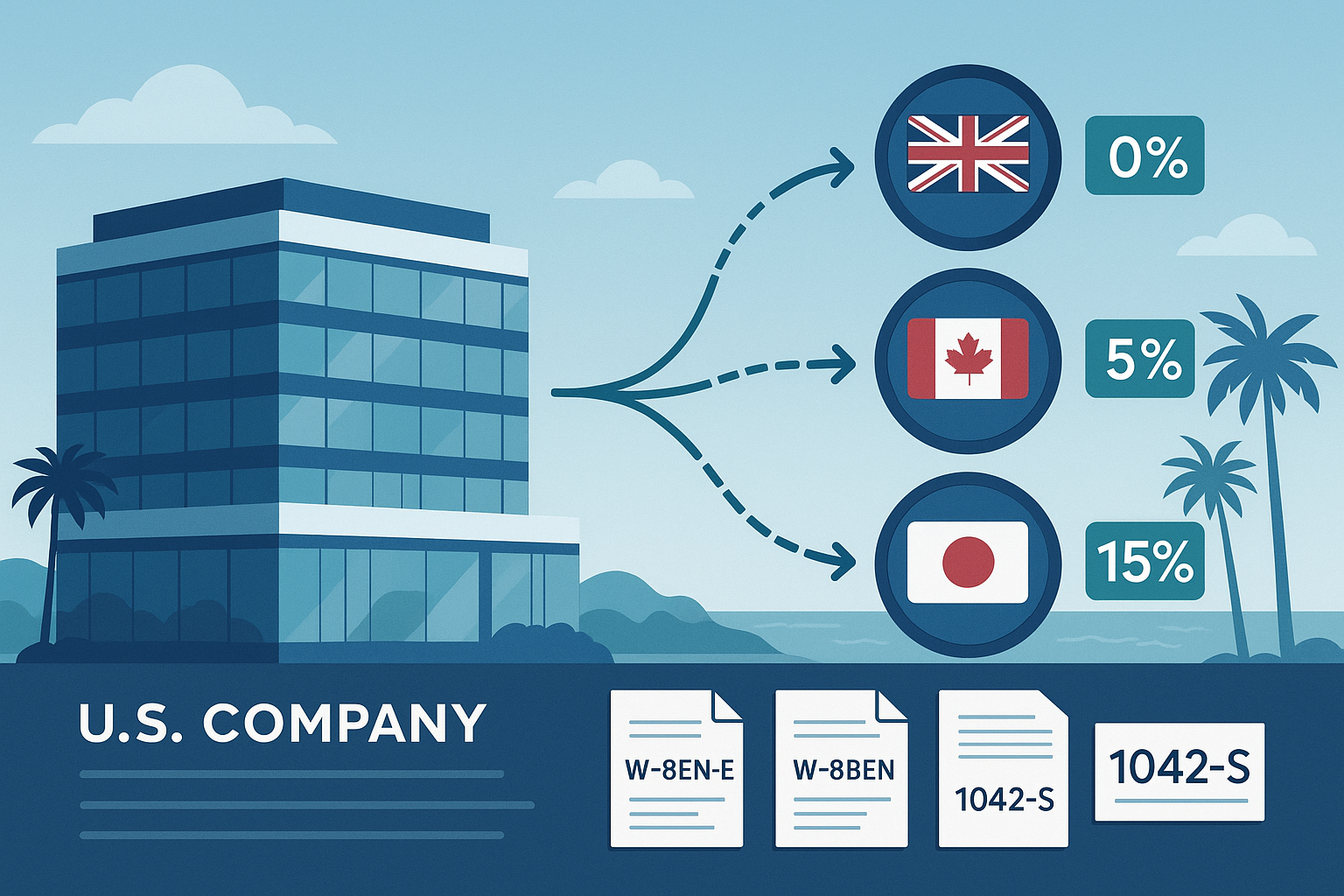

Use the right form (W-8BEN, W-8BEN-E, W-8ECI, W-8EXP, W-8IMY) and validate capacity, treaty article claimed, LOB (limitation-on-benefits) test, and U.S. or foreign TIN requirements. An incomplete or expired W-8 = 30% default withholding.

✅Apply treaty rates the right way (“relief at source”).

Many U.S. income tax treaties reduce withholding on portfolio dividends (often to 15% and lower for substantial corporate owners) and reduce interest (often to 0% in modern treaties), if the investor qualifies under LOB rules. Document the treaty article, ownership thresholds, and beneficial-owner status in your files.

✅Consider the Portfolio Interest Exemption (PIE).

Properly documented portfolio interest (e.g., on registered obligations with no contingent interest features) is often exempt from withholding without a treaty. The W-8 must certify the beneficial owner meets PIE requirements.

✅Watch special cases.

REIT dividends, substitute dividends, contingent interest, and related-party financing can break preferred rates. Equity-linked “dividend equivalents” under §871(m) may trigger withholding even without an actual dividend.

✅Reconcile and report.

Withholding agents must deposit tax timely and file accurate Forms 1042/1042-S and Form 1042 annual reconciliation. Tie out payment files to 1042-S boxes, recipient codes, chapter 3 vs. chapter 4 status, and GIIN/FATCA classifications.

✅Know who the “withholding agent” is and the liability.

If you pay as an agent, intermediary, or platform, you are the withholding agent for U.S. tax purposes. That means you’re responsible for obtaining valid W-8s, applying treaty/PIE rates, withholding and depositing tax, and filing Forms 1042/1042-S. If you fail to withhold or report, the agent is liable for the tax, as well as potential penalties and interest. Contract terms with the payee don’t shift this obligation. Build this responsibility into your onboarding and payment workflows.

San Diego perspective:

We frequently help Carlsbad and greater San Diego companies set up clean onboarding and run quarter-end 1042-S checks so there are no year-end surprises.

Contact us for a consultation.

info@usibts.com

760-842-7885

Share this post :

Categories